What's crypto's version of the S&P 500?

Or, constructing a capitalization-weighted cryptocurrency index

I’ll inaugurate this crypto blog by coming right out and saying it: trying to time the crypto market is usually a spectacularly bad idea.

I mean, yes, there’s the story of that investor who bought $3400 of Shiba Inu coins in August 2020 and saw their holdings appreciate to $1.55 billion in October of this year, a cool 450,000x return.

But let’s be honest, the average Joe had never heard about Shiba Inu back then, and the coin was doing maybe $2000 in volume a day. If you had $3400 to invest back then, you almost certainly would not have bought Shiba Inu1.

A more likely outcome is that you would have bought SHIB back when its hype cycle was in full swing this October — and had you bought it at its peak, you’d currently be down by 66%.

Get-poor-quick schemes

Speaking from experience, I too seem to have exquisitely bad timing at buying crypto coins. I bought Chainlink at its peak (down 60+%), Uniswap at its peak (also down 60+%), Olympus DAO at its near-peak (down 70+%), and Klima DAO at the very zenith of its Twitter hype cycle (down 90+%). Good thing I only tossed a few bucks in, but this all reminds me of that tongue-in-cheek “ETF” that makes the opposite trades of this popular tech pundit and has handily beat the S&P 500.

(The good news, I suppose, is that I avoided investing in this project called SquidGodFinance, whose price peaked at $1300 and then collapsed to like $20 before it became so obscure that everyone stopped tracking it. As a sort of “where are they now”, the project has now rebranded to Stargate and is offering a Ponzi-to-end-all-Ponzis APY of almost 17 million percent. That’s one way to beat inflation, I guess.)

Point being, there’s a reason why stock market investors buy index funds. I’m always the first person to tell people that you can’t beat the market (unless you have insider information, but that’s another story), so you shouldn’t hold individual stocks. And since the market follows a random walk in the short run, your best bet is to stop actively trading and hold (er, HODL) index funds for the long haul. But why does nobody seem to apply that logic to the crypto-verse?

Constructing a crypto index

Before we even think about crypto index funds, we have to talk about the actual index that the fund tracks — like the NASDAQ index that the famous QQQ fund tracks. In stock markets, the value of the index is plastered everywhere, but crypto media and exchanges are oddly quiet on that front. The closest thing I’ve seen is how Coinbase compares a coin’s performance to the broader “market,” but they don’t explain where that number came from:

So, I thought it’d be instructive to compute a crypto index myself and share the results.

As a review, indices are usually capitalization-weighted,2 so you just sum up the market caps of all the companies you want to track (usually the N largest in a certain sector) and divide by some constant to make the number more tractable.

The first problem you run into when trying to compute a crypto index is that market cap is considered a pretty useless metric for cryptocurrencies. It measures neither the amount of money that went into the system nor the amount of money that can be extracted from it; if everyone tried to sell their Bitcoin at once, the price would crash, and they’d get much less than the nominal market cap. The classic proof of why market cap is misleading goes thusly: if I mint a trillion of some random new coin, then sell one coin to myself for $1, then my coin will have a $1 trillion market cap, which is more than Bitcoin’s at the time of writing.

I might write more thoroughly about crypto market caps later, but suffice to say that nobody can think of a better metric than market cap. And because the crypto media fixates so much on market cap, it’s useful for observers to pay attention to it in an intersubjective reality type of way.

Methodology (and the GitHub)

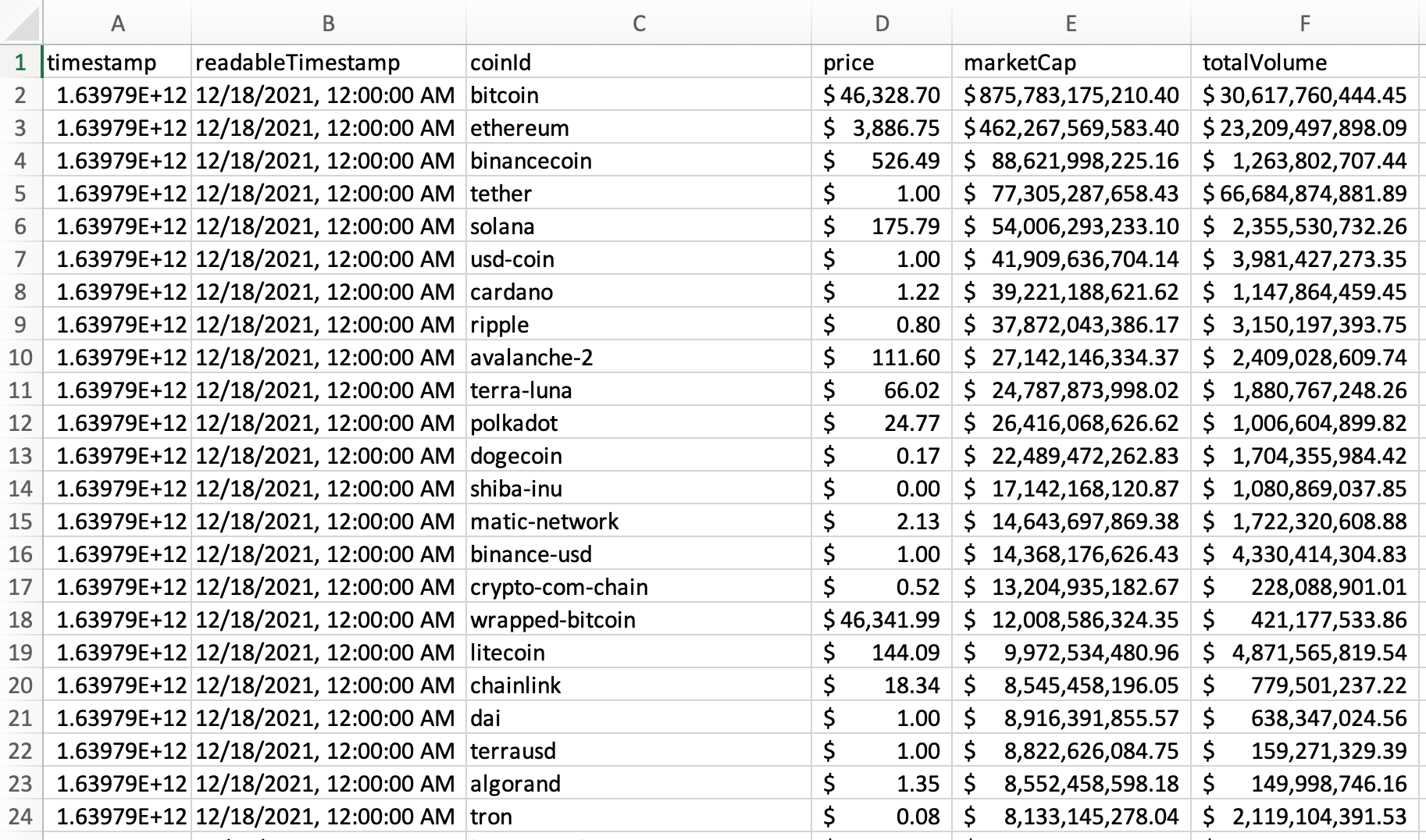

Anyway, lacking any better alternatives, I went with market cap. So I used CoinGecko’s API and pulled data on the top 500 cryptocurrencies by market cap. This list might seem hilariously out-of-date by the time you read this post, but at the time it was a pretty decent approximation of the most relevant coins.

Then I excluded all the stablecoins (Tether, USDC, etc.) and the derivative coins (the Ethereum-wrapped and Compound-wrapped ones, the ones pegged to the prices of other coins, the insane ones that are 2x-leveraged versions of popular coins,3 etc.), since those aren’t relevant to analysis of “fundamental” crypto assets.

For the remaining 453 coins, I pulled historical price and market cap data for the last 365 days. After some data processing, I had a ranked list of the 453 biggest coins for each day in the past year.

(If you’re keen on it, check out the GitHub repo — it’s not very polished, but the code and data are all there.)

Results, and a graph

The last step is choosing how many coins you want to include in the index. You could focus only on the large-cap assets — like how the S&P 500 covers only the 500 biggest American companies — or expand to include smaller ones too — like the S&P 1500, which covers the top 1500 companies. (The caveat is that, since big companies have so much more market cap than the small ones, the long tail of companies in these “total market” indices don’t actually contribute that much.)

Since I had all the data, I figured I’d compare the top 10, 20, 50, 100, 200, and 500 (well, 453) indices to see what shook out. I threw in Bitcoin’s performance (which is a top-1 index, in a sense) as a comparison. Pretty interesting results:

Three things we can learn

As I mentioned before, the long tail of small-cap assets is thoroughly swamped by big-cap assets, so they don’t contribute that much. So it’s no surprise that the indices all moved in tandem over the last year.

But what surprised me is that, the more coins you included in the index, the better it performed! The lines are thick on the graph so it’s hard to pick it out, but on the last day I picked, the top-10 index was at 2.92x its value from a year prior, the top-20 at 2.99x, the top-50 at 3.08x, the top-100 at 3.16x, the top-200 at 3.22x, and the top-500 at 3.29x. The same trend showed up throughout the year; this shows up on the graph as the teal line (“Top500”) always sitting at the top of the stack and the red and blue lines (“Top20” and “Top10” respectively) sitting at the bottom.

This goes to show that the smaller “altcoins” are doing much, much better than the big “blue-chip” ones — remember that the small ones make barely any contribution to the overall index, so the fact that there’s still a significant divergence shows just how hefty their advantage is. (At some point I should construct a mid-cap and small-cap index, kind of like the S&P 400 or S&P 600.)

Another thing to realize is that the graph is still really spiky; had you bought the index at its peak in May you’d have been down almost 50% come July. Portfolio theory tells us that diversifying your portfolio removes idiosyncratic risk and leaves you with just the market’s underlying risk — and this index shows us what that underlying risk profile is. It should come as no surprise that crypto is high-risk, high-reward. That’s just the nature of the beast.

Finally, I was also surprised to see just how quickly the market caps drop off. Only two coins have market caps over $100 billion; once you get past #17 you fall below the $10 billion mark; once you get past #71 you’re below $2 billion. As egalitarian as crypto might sound, there’s a lot of clustering at the very top, and the overall market is still very small in the grand scheme of things. My hypothetical “mid-cap” index might start around #10 and the “small-cap” index might start around #50. Compare that to the US market, where mid-caps start after #500 and small-caps start after #900 (according to S&P, at least).

“The Moon & Rug 500”

The last thing I need is to give this index a catchy name. Let me know if you think of anything better, but for now I’m calling it the “Moon & Rug” as a play on “Standard & Poor’s.” To the uninitiated, “moon” is crypto slang for coins exploding in value, while “rug” (short for “rug pull”) refers to scams where investors lose all their money. What better description for the wildly divergent outcomes in crypto than “moon” and “rug”?

(Plus, I always thought it was funny that the “P” in “S&P” stands for “Poor’s.” Ironic name for a financial instrument that’s supposed to be about building wealth. Hence the usage of “Rug” as the second item in the “M&R” pair.)

So, we can nickname our indices “The Moon & Rug 10,” “The M&R 20,” etc. Maybe I’ll eventually put up a website where people can track these.

Constructing an M&R index fund

Indices are useful as benchmarks for the performance of various individual assets, but they really shine when they’re used as the basis for index funds. There are a lot of mechanics that go into making a fund — notably rebalancing — so I’ll probably dig into that later.

And it seems like interest in crypto index funds is picking up; there was even a piece about decentralized index funds in Bloomberg this morning.

The question that’s most relevant for this discussion is, which Moon & Rug index would we want to use to construct an index fund? On the one hand, we might want to have a giant fund that includes all 500 (well, 453) of the top coins, since that’s had the best performance. But there are some downsides to having such a broad fund:

The more assets you have to manage, the more cumbersome portfolio management is, especially rebalancing. That will probably lead to higher cost bases.

Some crypto exchanges charge you a fixed fee for each transaction,4 so making a lot of small purchases will rack up a lot of fees. It’s more efficient to buy a large quantity of a small number of coins.

The more popular coins can be invested to earn returns, such as through staking, liquidity pools, or various lending-and-borrowing platforms. These only provide like 4-8% APY, but it’s better than nothing. The more of your money goes toward the big coins, the more money you’ll be earning interest on. If you spread your money too thin, most of your capital will be tied up in tiny coins that you can’t earn interest on, and so your dividends will be worse.

Smaller coins usually have lower trading volumes, so it’s very possible that your obscure coins’ value will increase but you won’t actually be able to cash them out.

So, if we were constructing a Moon & Rug index fund, we’d probably want to strike a balance — perhaps we’d focus on the M&R 20 or the M&R 50. (There’s some precedent for this: most crypto index funds out there are opaque about their composition, but the Crypto20 one is, as you might expect, based on just the top 20 coins.)

Extensions

So that’s the core of the idea — how you’d compute, analyze, and use a capitalization-weighted crypto index. There are all kinds of other financial products you could create next: an equal-weighted index, a mid-cap or small-cap index (as I mentioned earlier), an industry-specific ETF that covers things like metaverse tokens or “Ethereum killers”, and so on. I’m not sure what I’ll use this blog for, but I might dive into how we’d construct those indices.

There are also some philosophical tensions to unpack. The kinds of people who have historically bought crypto are the exact kinds of people who wouldn’t buy index funds, but as more casual investors (and the institutional investors who are always hovering around the crypto space) come into the fold, that might be changing. And perhaps there’s something nihilistic about treating cryptocurrencies as nothing more than financial instruments, overlooking all the other things they claim they can do. That also looks like fertile ground for future discussion.

But for now, I know I’d be the first person in line for a fund based off our Moon & Rug index. As they say:

Time in the market beats timing the market.

Thanks for reading.

This is why I’m so annoyed by those “If You Had Bought $100 of [RandomCoin] A Long Time Ago, Here’s How Much You’d Have Now” articles that the financial press churns out on a daily basis. You probably never would have bought the coin at that time anyway!

The Dow Jones being a notable exception — it just averages up the stock prices of all its constituents, which is dumb because a smaller company whose stock is at $1000 should not count for ten times as much as a huge company whose stock is at $100.

Initially I was surprised that people would want even more risk than the normal crypto markets provide, but then I learned that there are people who gamble on 100x-leveraged Bitcoin futures, so 2x seems tame by comparison.

Other exchanges charge you a percent of your overall transaction, so doing small transactions isn’t a big deal. But shuffling money between wallets and trading platforms always has a fixed fee, so this remains an issue.

Love this! How do I invest in Moon & Rug 500?