The curious case of second-tier stablecoins

A tale of monetary policy, algorithmic stablecoins, crypto ghost towns, animal spirits, intersubjective reality... and corgis.

While I was researching how to build a cryptocurrency index, I had the chance to look through almost 2500 of the top cryptocurrencies, and boy were there some bizarre creatures in this zoo. I discovered the delightfully-named The Corgi Of Polkabridge; the ridiculous 3x-leveraged Ethereum coin (not as bad as 100x-leveraged Bitcoin futures, I guess?); the unusual “fan tokens” themed after European football clubs like FC Barcelona; several dog-themed Inu coins (including Zombie Inu); a few interesting pseudo-index funds like the Metaverse NFT Index1 (it actually tracks the metaverse hype pretty well); and more.

Jokes aside, the reason I bring this up — and the reason we’re taking a quick detour from the crypto index funds series — is that there’s one class of coins that really surprised me during this trawl through the long-tail of cryptocurrencies.

Those are the stablecoins, the ones nominally pegged to the dollar or Euro or what have you. But I’m not talking about the well-documented woes of Tether or about the other famous stablecoins like USDC.

Rather, I’m talking about the little-documented world of second-tier stablecoins. Buckle up, and we’ll meet three of these coins — besides being fun to look at, they’ll give us a chance to tour some lesser-known parts of the crypto world and touch on questions of governance, economics, institutions, psychology, intersubjective reality, and more.

USDX and why everyone’s got their own stablecoin

If you were in the fortunate position of being able to found your own country, one big decision you’d face would be the one of currency. You’d need a currency to organize your economy, and you could either run your own currency or effectively use someone else’s (either by pegging to a more established currency or just using their currency outright). While the latter two options are easier to implement, they make it much harder for you to control the economy with tools like monetary policy, especially since you need to have a huge pile of another country’s currency on hand at all times.

Many DeFi projects face an analogous problem. Whether you’re lending money, accepting cash deposits, enabling coin trading, establishing an endowment, or doing other DeFi tasks, you’ll need some common base currency that everyone will be happy to accept. Bitcoin, Ethereum, and other “blue-chip” coins are nice but still too volatile. You could offer your own made-up proprietary currency, but it has no “inherent value,” so many people wouldn’t want to accept it. Instead, you can turn to stablecoins, which everyone agrees have a consistent value.2

You could use well-known stablecoins like USDT, but like a new country, you wouldn’t be able to mint or “burn” coins at will, and you’d need to keep a massive war chest of those coins to ensure everyone can get some. This is a pain, so many DeFi projects decide to run their own stablecoins instead.

This leads us to the first interesting stablecoin, USDX (currently ranked around #370 by market cap). It’s run by a DeFi group called Kava, which lets you borrow and lend USDX coins, among other things. This coin has had an interesting history: it’s supposed to be valued at $1 exactly, but for a while it stumbled around in the 80-90¢ range — until it got its act together last July. It’s hung around $1 ever since, though it’s currently a few cents shy of that (98¢).

One challenge with running your own stablecoin is that you have to back each 1 token with at least $1 of assets (at least, you should… Tether doesn’t). Kava apparently backs each USDX coin with at least $1 of crypto. So it appears that, for a while, Kava either hadn’t sufficiently backed their coin, or people didn’t believe that they had.

Dynamic Set Dollar, “algorithmic stablecoins,” and breaking the buck

Let’s move on to the second coin. In the normal world of finance, money market funds are super-low-risk mutual funds that are supposed to trade at exactly $1; unlike a bank account, they put your money into stable government securities and give you a slightly better interest rate (though these days it’s practically zero). Anyway, if a money market fund “breaks the buck,” it’s considered catastrophic — back in 2008, when the banks were failing, some mutual funds fell as far as 96 or 97 cents.

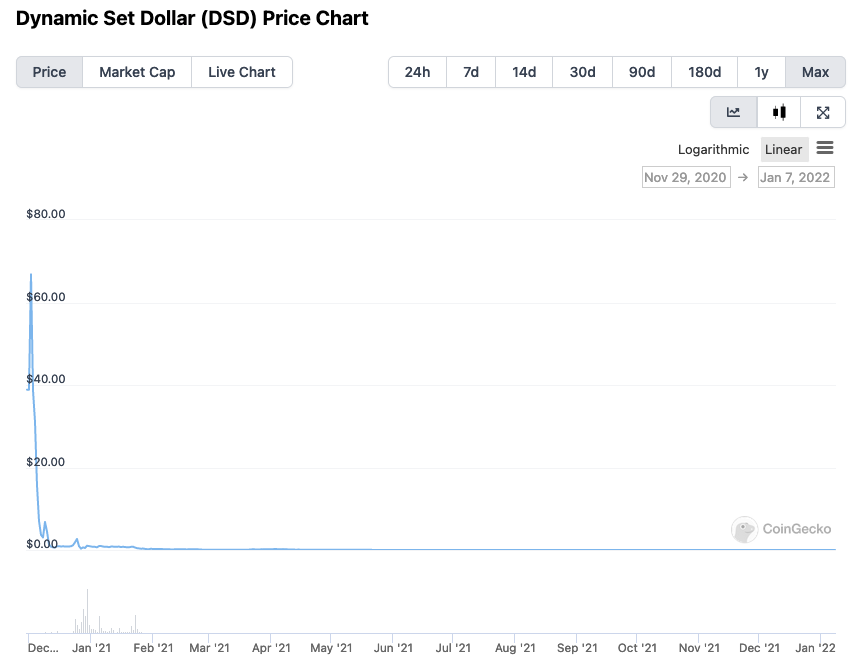

As I looked through the long tail of stablecoins, I found several that had broken the buck in… slightly more dramatic fashion. I hereby introduce the Dynamic Set Dollar ($DSD). It was about the 90th-biggest coin in early 2021, but it’s not doing so well nowadays:

Yes: bizarrely enough, this supposed stablecoin started out its life by spiking to over $60 (apparently its intraday high was once almost $87). It hung out around 80¢ for a while, then it broke the buck even further by collapsing to its current value of just 0.3¢. That’s 99.7% less than a dollar, and 99.997% off its all-time high. It’s sitting around #2600 by market cap.

I’m not really sure what happened, but the gist is that this coin is a so-called “algorithmic stablecoin,” which attempts to back its peg using a collection of assets that are gathered and stored in a decentralized way, rather than by a large centralized entity (such as the companies behind Tether or USDC). Algorithmic stablecoins are usually backed by a DAO that coordinates the pegging and conducts monetary policy.

In this case, the DAO behind the Dynamic Set Dollar is some strange kitchen sink of a bunch of DeFi products — staking, bonding, liquidity pools, yield farming, you name it —and I get the feeling that everyone just abandoned the project. It seems like everyone who was buying debt or “locking” assets just took their money and walked away at a certain point; you can explore the history here (look around epoch 600 to 700). [Edit: apparently, that page has stopped working since I published… fitting.]

The moral of the story is that throwing an algorithm at a governance problem isn’t necessary going to solve it — without people to steer the ship and provide the funds, any algorithmic project will dry up and fail. It’s like any human institution: without people to run it, all the fancy bylaws and machinery will eventually grind to a halt.

I think there’s a lot to learn from these “ghost-town” crypto projects. You only hear about the success cases, as it were; what about all the DAOs and DeFi groups that folded? (Fortunately, the ConstitutionDAO epilogue seems to have broken through to the mainstream media.)

Steem Dollars and intersubjective reality

So far, we’ve seen a struggling proprietary stablecoin and an abandonware algorithmic stablecoin. Those were interesting, but this last one is my personal favorite. This one’s called the Steem Dollar ($SBD), currently ranked around #630 by market cap.

Before we check out the graph, a bit of backstory. Steem is a relatively long-tenured crypto project, stretching back over 5 years; it’s a platform that powers decentralized social media apps like Steemit (a blogging platform and perhaps their best-known product) and a decentralized YouTube clone. The Steem Dollar is the platform’s proprietary stablecoin, similar to Kava’s.

Anyway, the graph is what makes this project so fascinating:

The first thing you probably notice are the two massive “mountain ranges,” which correspond to the Steem Dollar breaking the buck during the late-2017 crypto boom and the current 2020–2022 crypto boom. There’s also a smaller “hill” in early 2017. But what’s so interesting is that the coin’s price actually went above $1 — quite far above. It broke the buck, but in the opposite direction!

Even weirder, after the coin went berserk in 2017 and ‘18, it calmed down and traded at around a dollar for the better part of two years… after which point it suddenly started behaving wildly again. Dr. Jekyll and Mr. Hyde, anyone?

I’m not entirely sure what went on here, but a useful thing to realize here is that the price of a crypto asset is often completely untethered from its “real” value. Sure, this coin might have had $1 of backing (its Net Asset Value, in mutual fund-speak), but that doesn’t necessarily mean that the coin had to trade at $1. Many stablecoins can’t be easily traded for real money, so that arbitraging force you might expect (where someone could buy a bunch of coins for $1 at the treasury and sell them for, say, $2 on the open market, dragging the price back down to $1) wouldn’t be there. Therefore, there’s no mathematical force bringing the price of the coin back to its “proper” value.

More often, the thing keeping a stablecoin at $1 is Yuval Noah Harari’s intersubjective reality, the same force that helps give fiat currency its value.3 Everyone thinks the coin should be worth $1, so that’s what its value stays at.4

But intersubjective reality is fickle. If everyone starts thinking that the stablecoin is worth something else, then, well… it will be! I think that’s what happened to the Steem Dollar: during the crypto booms, some people started to spread the meme that the coin was actually going to go “to the moon” despite being a nominal stablecoin, so the coin’s price started fluctuating to reflect that new intersubjective reality. Perhaps some market manipulator bought a bunch of coins at $1 and sold them back to themselves at $15 back in 2017, thus triggering a stampede as everyone sought to cash in on the new meme. But the meme eventually faded out, reflected in the gradual slumping back down to $1.

I’m not sure what’s going on, but one thing’s for sure: it’s more predicted by investor psychology than hard math and economics. This is what economists refer to as the “animal spirits” of the market: the emotional and seemingly-irrational actions of investors lead to actual changes in the ground truth. It’s similar to the concept of “castles in the air” from the classic book A Random Walk Down Wall Street5: there’s no foundation, but that doesn’t stop people from building on top of what everyone else has already built. Intrinsic value does not determine the price of assets like these — psychology does.

In the normal stock market, where there’s more “ground-truthing” in the form of earnings calls and whatnot, I think there are at least some factors that pull prices toward some rational value. In the abstract world of crypto, all bets are off, and animal spirits rule the day. One day a stablecoin is the latest memecoin; the next day, it’s a sober dollar-a-pop coin; the next day, it’s a booming asset yet again.

What it all means

The reason I tell these stories isn’t that these coins are market movers — rather, they’re quite obscure. Instead, it’s to remind us that crypto does not work in the clean and rational way we might expect — where coins pegged at $1 always trade at $1, algorithms can run forever without intervention, and “intrinsic value” rules the day. We live in a strange and complex world made by, for, and of humans, and crypto is a reflection of that reality.

Thanks for reading. I’ll see you next time.

Oh, geez, now I learned that you can swap this coin ($PLAY) for the $DOUGH coin on a decentralized exchange. $PLAY–$DOUGH.

More irony. The most reliable cryptocurrencies are the ones that maintain close ties to fiat.

That, and the fact that the government collects taxes in the fiat curency.

I haven’t fully fleshed out this theory, but I think the fact that Tether isn’t fully backed isn’t the big risk factor for Tether. It’s very hard to exchange Tethers for US dollars anyway. The thing keeping Tether at $1 is the intersubjective reality and the fact that various third-party institutions honor the 1 Tether = 1 USD exchange rate. Those can change on a dime, though, and that’s what should make Tether worry.

Great book, by the way. Definitely read it if you’re a keen crypto observer.